Ontario pensions and retirement savings

What you need to know about the retirement income system in Ontario, including how it works, challenges for the future and what you can do to help maintain your standard of living in retirement.

Understanding the retirement income system

Evidence shows that many Ontarians are not saving enough to maintain their standard of living in retirement. Beyond the statistics, many feel insecure and uncertain about their financial future.

It’s important to learn how the retirement income system works, so that you and your family can have the retirement security you deserve.

Retirement income

The Canadian retirement income system is typically described as having three parts:

-

Old Age Security (OAS) and the Guaranteed Income Supplement (GIS). OAS provides a monthly benefit to almost all Canadians when they reach age 65. GIS provides supplemental income to Canadians who have low retirement incomes.

-

Canada Pension Plan (CPP) provides a monthly benefit to people who have contributed to this publicly-administered plan over the course of their working lives.

-

Personal Savings and Workplace Pension Plans. Workplace pension plans are privately administered by employers who choose to offer them. Personal savings can include Registered Retirement Savings Plans (RRSPs), savings accounts, investments and home equity.

These combine to fund your retirement, but the importance of each one may differ depending on your personal circumstances.

How much you should save

Retirement experts suggest that households should aim to have 50-70% of their pre-retirement income for living expenses in retirement.

For example, assuming you want to replace 70% of your pre-retirement income:

-

If your annual pre-retirement income is $20,000 per year: your standard of living in retirement will likely be maintained by OAS and CPP income, even without additional income from savings.

-

If your annual pre-retirement income is $40,000 per year: in addition to OAS and CPP income, you would need an additional $11,795 per year, which must come from your personal savings and/or workplace pension plans to maintain your standard of living in retirement.

-

If your annual pre-retirement income is $75,000 per year: in addition to OAS and CPP income, you would need an additional $33,329 per year, which must come from your personal savings and/or workplace pension plans to maintain your standard of living in retirement.

Challenges for the future

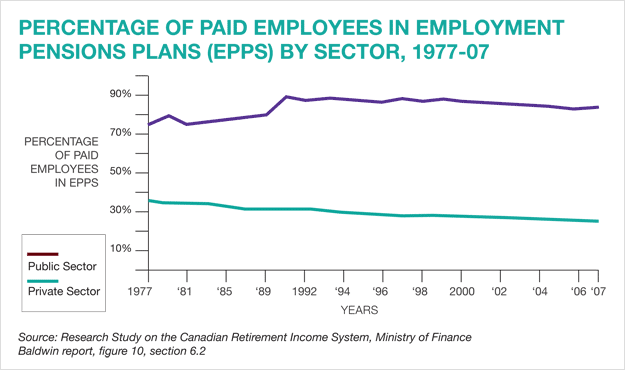

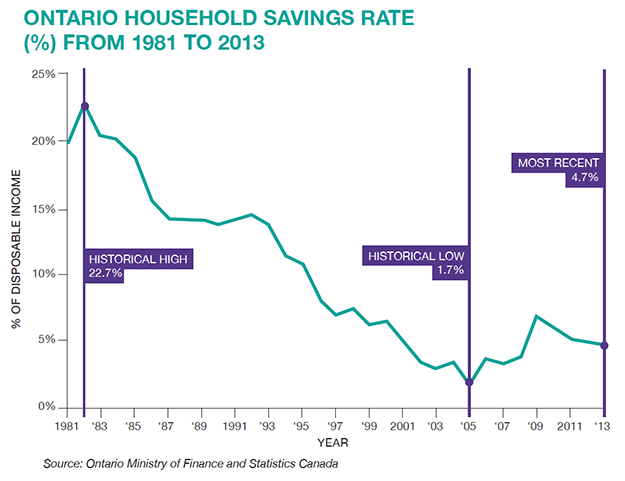

Fewer pensions, lower savings

The number of workers enrolled in a workplace pension plan is steadily declining, and personal savings by Ontarians have decreased over the past 30 years.

Consequences

For households not contributing enough to their personal savings (see Table 1 below), this means:

- The income provided through the CPP and OAS may not be enough to maintain their standard of living in retirement. As a result, a drop in the household’s standard of living may occur.

Other challenges

Other pension challenges we will face in the future include:

-

Increasing life expectancy: the number of years that a person will live after age 65 has increased significantly. This has put pressure on pension plans and personal savings to provide retirees with enough income to maintain their standard of living.

-

Pressure on younger workers: if many future retirees do not have adequate incomes, younger workers will bear the cost burden, either through higher taxes to support programs for seniors or through direct financial support of older family members.

-

Government spending: inadequate retirement savings will put pressures on federal and provincial resources funded by taxpayers.