Building together – Guide for municipal asset management plans

This guide explains the importance and the features of an asset management plan for municipal officials with descriptions and examples.

Letter from the Minister of Infrastructure and Minister of Transportation

Infrastructure investments are vital to strengthening the economy, creating jobs and building strong communities in which residents enjoy a high quality of life.

That’s why the Ontario government has invested more than $75 billion in infrastructure since 2003 to support our hospitals, schools, transit and roads – creating or preserving close to 100,000 jobs, on average, each year.

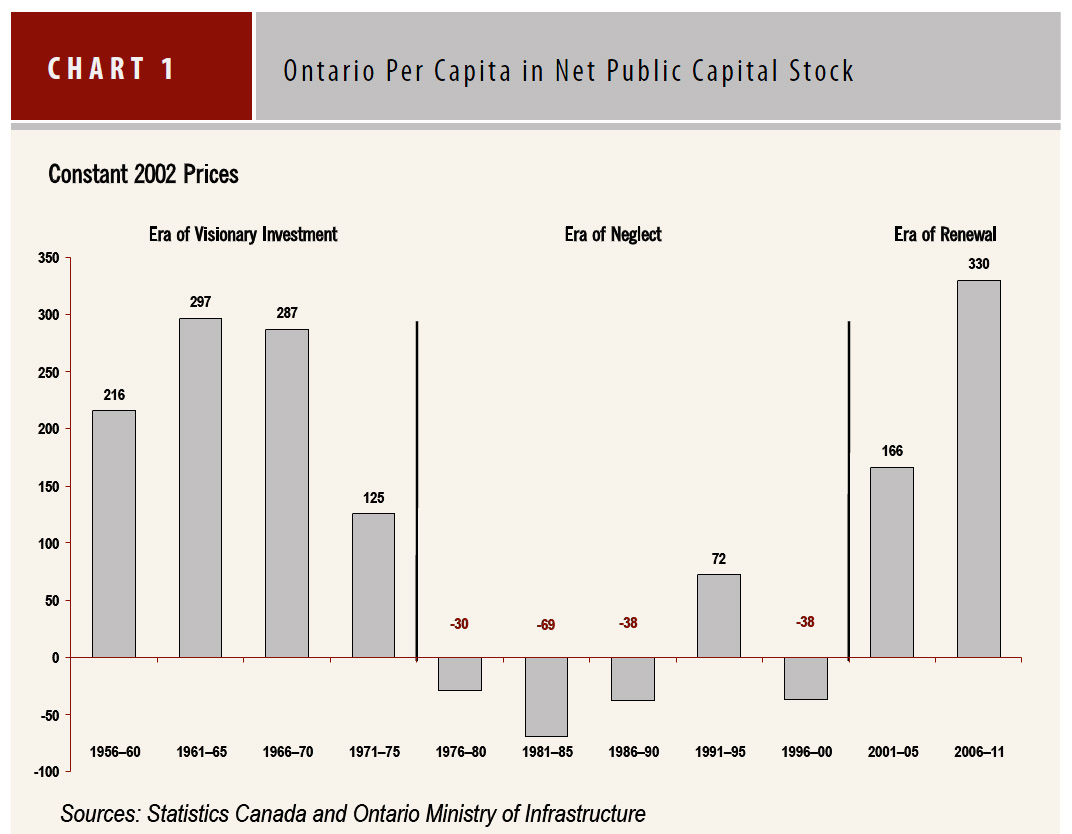

Chart 1: Ontario Per Capita in Net Public Capital Stock

Sources: Statistics Canada and Ontario Ministry of Infrastructure

Last June, we released our 10-year infrastructure plan, Building Together. This plan is the first of its kind and reinforces our strong commitment to continued investment in infrastructure.

Despite significant fiscal challenges, we are standing by that commitment. In the 2012 Ontario Budget, we committed to invest more than $35 billion in infrastructure over the next three years. We are also standing by our commitments to municipalities, including honouring our commitment to implement the uploads agreed upon through the Provincial-Municipal Fiscal and Service Delivery Review (PMFSDR) according to the schedule agreed upon through the PMFSDR, and providing over $1.8 billion to municipalities through the combined benefit of both the Ontario Municipal Partnership Fund (OMPF) grants and provincial uploads in 2012.

Recognizing that we have more work to do with municipalities and the federal government to address municipal infrastructure challenges, the government committed through Building Together to develop a municipal infrastructure strategy.

Asset management will be the foundation of the strategy. Asset management planning will allow needs to be prioritized over wants. It will help ensure that investments are made at the right time to minimize future repair and rehabilitation costs and maintain municipal assets.

We are moving toward standardization and consistency in municipal asset management. The first step is requiring any municipality seeking provincial capital funding to prepare a detailed asset management plan and show how its proposed project fits within it. As part of this process, municipalities will need to demonstrate how they themselves are assisting financially with the proposed project, including engaging with Infrastructure Ontario.

We have heard loud and clear that some municipalities, particularly small ones, struggle with the task of preparing detailed asset management plans due to a lack of in-house technical capacity or limited financial resources.

The government will therefore be making funding available on an entitlement basis to approximately 350 communities to assist with the preparation of asset management plans. We are taking an entitlement approach so municipalities can focus on improving their asset management plans rather than on competing for funding.

This guide is part of a toolkit to help municipalities prepare asset management plans and consider all the resources that are available to help address infrastructure needs. This web-based toolkit will also help us learn from each other by providing a forum to share best practices and success stories.

The goals of the municipal infrastructure strategy include: making good asset management planning universal; moving toward optimal use of a full range of infrastructure financing tools; and addressing the structural challenges facing small communities.

The federal government should be a key partner in this effort. We are actively participating in the federal government’s year-long engagement process to inform its long-term infrastructure plan. We have been emphasizing our commitment to asset management and smart investment.

We will continue to work with our municipal and federal partners to address municipal infrastructure challenges and ensure Ontario’s future prosperity.

Bob Chiarelli

Minister of Infrastructure,

Minister of Transportation

Part 1: Context

Introduction

Public infrastructure is central to our prosperity and our quality of life. That is why the province released Building Together, a long-term infrastructure plan for Ontario, in June 2011. Building Together responds to the far-reaching trends that will affect Ontario’s infrastructure needs, including a more global and service-oriented economy; a larger, older and more urbanized population; and the effects of a changing climate. The plan sets out a strategic framework that will guide future investments in ways that support economic growth, are fiscally responsible, and respond to changing needs. A key element of this framework is ensuring good stewardship through proper asset management.

Municipalities deliver many of the services that are critical to Ontarians, and these services rely on well-planned, well-built and well-maintained infrastructure. For example, municipalities are responsible for more than 15,000 bridges and large culverts and more than 140,000 kilometres of roads that support the movement of people and goods. In addition, more than 10 million Ontarians depend on municipal water and/or wastewater services.

The province, municipalities and the federal government share an obligation to address municipal infrastructure challenges. The province takes this obligation seriously. Since 2003, the province has invested approximately $13 billion in municipal infrastructure. This includes more than $1.8 billion that went towards municipal and community infrastructure stimulus projects in the wake of the 2008 economic downturn. These investments have helped municipalities to modernize and expand transit systems, repair and upgrade roads and bridges, improve water and wastewater treatment, and revitalize community infrastructure.

In addition, since 2003, the Infrastructure Ontario Loan Program has provided financing to eligible public sector clients to help renew infrastructure and deliver value to the public. The Loan Program borrows on behalf of municipalities and other eligible public organizations, allowing smaller borrowers to secure financing at more favourable interest rates than would otherwise be available to them.

To date, the Loan Program has approved and executed more than $5.8 billion in affordable loans – including some $4 billion to 215 municipal clients to help support more than 1,500 projects. These projects include important investments in roads, bridges, and water/ wastewater systems across the province.

Provincial funding and financing for municipal infrastructure is complemented by other ongoing municipal support initiatives. These initiatives include the uploads agreed upon through the Provincial-Municipal Fiscal and Service Delivery Review (PMFSDR), which will ensure that more property tax dollars are available for important municipal priorities — including investments in infrastructure, funding provided through the Ontario Municipal Partnership Fund (OMPF), and others. The province’s ongoing support to municipalities has increased to $3.2 billion in 2012 – almost three times what was provided in 2003.

Municipal infrastructure strategy

Despite significant investments by all orders of government, more needs to be done to address current and emerging municipal infrastructure needs. That is why the province committed through Building Together to work with municipalities and the federal government to establish a municipal infrastructure strategy.

What will the strategy do

A long-term, cooperative effort among all three orders of government will be required to address the challenges of current and emerging municipal infrastructure needs. The strategy will be guided by the following principles:

- Municipalities are the stewards of the infrastructure they own. The province and the federal government have an obligation to help municipalities address infrastructure challenges.

- Comprehensive asset management plans should guide investment decisions.

- Those who benefit directly from municipal infrastructure should pay for the service, whenever feasible.

- Opportunities should be pursued to provide infrastructure more efficiently by forging partnerships with other communities or consolidating services where possible.

- Maintaining roads, bridges, water, wastewater and social housing should be a top priority.

- Some communities face unique challenges that require tailored solutions.

- Infrastructure Ontario and the private sector can help address municipal infrastructure challenges.

As part of the strategy, policy activities in the following three areas will need to be discussed:

- Making asset management planning and public reporting universal.

- Making optimal use of the full range of budgeting and infrastructure financing tools.

- Addressing the structural challenges that are confronting small municipalities.

To minimize the reporting burden associated with asset management planning, the province intends to move toward a “one window” approach, which means that a single comprehensive plan would satisfy all provincial requirements related to municipal asset management. This will help streamline activities such as potential future regulations under the Water Opportunities Act, 2010.

What is the first step

Resolving municipal infrastructure challenges begins with improved asset management. The province views this as a prerequisite for a productive discussion about solutions, including permanent funding for municipal infrastructure.

In Building Together, the province stated that any municipality seeking provincial infrastructure funding must demonstrate how its proposed project fits within a detailed asset management plan. This will help ensure that limited resources are directed to the most critical needs.

What do detailed asset management plans need to include

Part Three of this guide sets out the information and analysis that municipal asset management plans should include, at a minimum. The province is moving in the direction of standardizing municipal asset management planning and this guide will help municipalities get a head start on developing detailed asset management plans.

Municipalities that already have detailed asset management plans do not need to replace them. Part Three of this guide can act as a template, but municipalities may select any appropriate format, so long as their plans include the information and analysis described in Part Three.

Financing strategies are a key component of a detailed asset management plan. Municipal councils must be open to all available revenue and financing tools. For example, there may be a need for some municipalities to revisit their “zero debt” policies. Debt financing, such as debentures, loans, and construction financing agreements, helps to spread the cost of expensive capital projects over time so that both current and future users of services share the burden.

In addition, some municipalities may need to revisit their policies regarding user fees, such as water rates. The prices of water and wastewater services in Ontario are low compared to many other jurisdictions and in many cases rates charged do not reflect the full cost of services.

The Commission on the Reform of Ontario’s Public Services, in its report on transforming Ontario’s public sector, discussed the need for full-cost water pricing:

“… in municipal water and wastewater services…stable investment over the long-term is more efficient and results in greater intergenerational fairness… Moreover, full-cost pricing in water and wastewater services has the added benefit of encouraging conservation — an area in which Canada desperately lags the world’s best. The electricity sector already operates on a cost recovery model; so too should water and wastewater services.

Recommendation 12-2: Implement full cost pricing for water and wastewater services.”

Source: Public Services for Ontarians: A Path to Sustainability and Excellence, Report of the Commission on the Reform of Ontario’s Public Services (2012).

As a condition of future provincial infrastructure funding, municipalities will be required to demonstrate that a full range of available financing and revenue generation tools has been explored.

Provincial infrastructure funding will continue to be conditional on municipalities demonstrating that they are complying with all relevant legislative requirements, including completing bridge inspections as required under the Public Transportation and Highway Improvement Act, 1990 and submitting Financial Information Returns as required under the Municipal Act, 2001.

Responsibility for the safety and maintenance of Ontario bridges is set out in the Public Transportation and Highway Improvement Act, 1990, Regulation 104-97, Standards for Bridges. The

Part 2: Asset Management Planning

Asset management in Ontario

What is asset management

Asset management planning is the process of making the best possible decisions regarding the building, operating, maintaining, renewing, replacing and disposing of infrastructure assets. The objective is to maximize benefits, manage risk, and provide satisfactory levels of service to the public in a sustainable manner. Asset management requires a thorough understanding of the characteristics and condition of infrastructure assets, as well as the service levels expected from them. It also involves setting strategic priorities to optimize decision making about when and how to proceed with investments. Finally, it requires the development of a financial plan, which is the most critical step in putting the plan into action.

Why is asset management so important

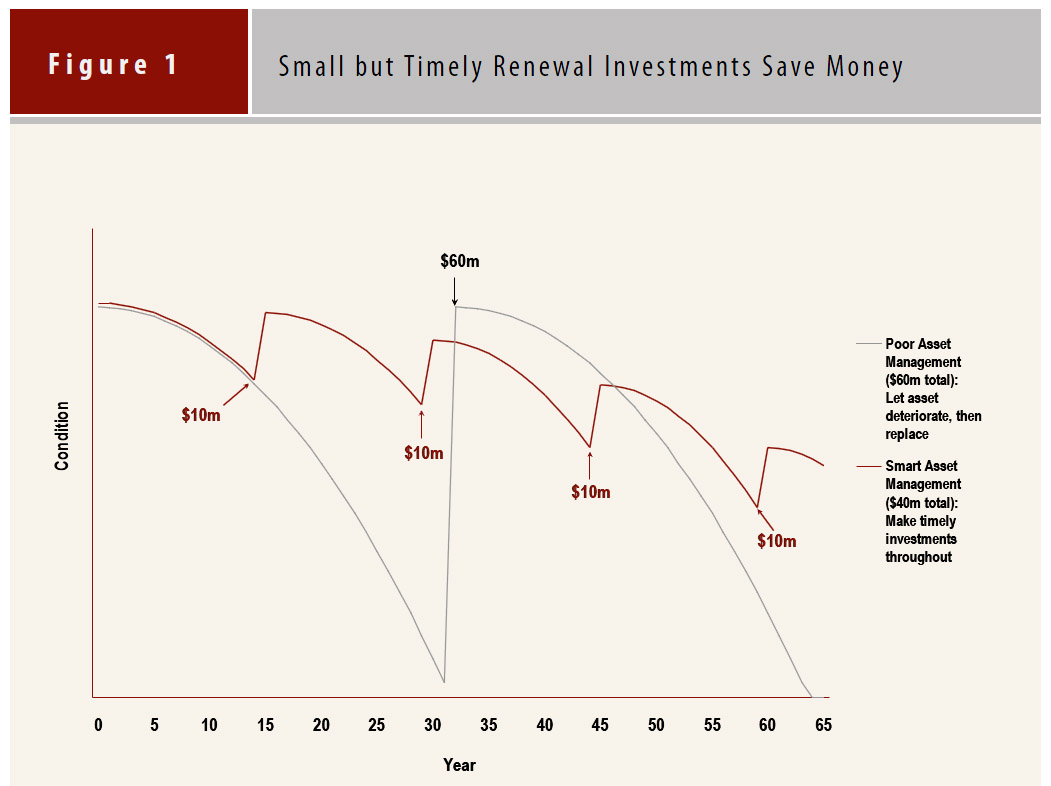

Because it takes a long-term perspective, good asset management can maximize the benefits provided by infrastructure. It also affords the opportunity to achieve cost savings by spotting deterioration early on and taking action to rehabilitate or renew the asset, as illustrated in Figure 1.

Figure 1: Small but Timely Renewal Investments Save Money

Good asset management is essential for all orders of government. It results in informed and strategically sound decisions that optimize investments, better manage risk — including the risk of infrastructure failure — and take into account the potential impact of other factors, such as climate change (e.g., damage due to extreme weather). For example, the Ministry of Transportation is increasingly applying preventative maintenance strategies to extend the life of pavements. Preventative treatments such as crack sealing, hot mix patching and thin surface applications help to maintain the pavement at a high level of service. When applied at the right time, these treatments can prolong pavement life up to 15 years, deferring the need for costly road reconstruction.

What is the current state of municipal asset management

Many Ontario municipalities, including the City of Thunder Bay, have made significant progress towards best practices in asset management.

However, there is more work to be done. Research undertaken in 2012 by the Ministry of Municipal Affairs and Housing suggests that fewer than 40% of Ontario municipalities have a long-term asset management plan in place for their capital assets.

Asset management in Thunder Bay

Thunder Bay’s infrastructure is aging while demand for better municipal services is growing in response to higher standards of safety, health, and environmental protection, and, to some degree, growth.

Beginning in 2004, the City’s Transportation & Works Department (now Infrastructure & Operations) reviewed its existing long range infrastructure strategies and current technical and financial practices. Staff compared the existing strategies and practices to best asset management practices in other municipalities and the InfraGuide prepared by the Federation of Canadian Municipalities, the National Research Council and Infrastructure Canada.

City staff produced an integrated asset management plan that identified ways to minimize life cycle costs and maintain adequate service levels at the lowest possible risk. From 2004 to 2011 capital funding increased. However the amount of funding required to implement the plan exceeded the established level of capital spending.

The 2011-2014 Strategic Plan approved by City Council supported an increase in capital financing capacity to reduce the annual infrastructure deficit and, in addition, requested administration to develop enhanced infrastructure funding options.

The Enhanced Infrastructure Renewal Program (EIRP) was approved by City Council and beginning in 2012, the EIRP was integrated into the budget process to address ongoing capital needs through incremental and dedicated property tax increases. By 2014, the gap between the amount of funding required to implement the City’s asset management plan and annual capital spending is expected to have been reduced by approximately 60%.

Source: Presentation to the Ontario Ministry of Municipal Affairs & Housing by Darrell Matson, City of Thunder Bay (February 2012)

What existing activities does asset management build on

While many municipalities need to improve their asset management practices, it is likely that most of them have a good foundation of information on which to build. The Ministry of Municipal Affairs and Housing’s research revealed that 84% of municipalities without formal asset management plans have protocols in place to manage/ prioritize assets. Such protocols can help contribute to the development of asset management plans.

One of the key outcomes of the Provincial-Municipal Fiscal and Service Delivery Review — undertaken by the Province, the Association of Municipalities of Ontario, and the City of Toronto — was the consensus that asset management planning is vitally important for addressing municipal infrastructure challenges. While there are costs associated with developing these plans, participants in the review agreed that such costs are generally repaid by the savings realized through timely and informed decisions.

Ontario municipalities have transitioned to accrual accounting — a critical first step in the development of asset management plans.

Accrual accounting and asset management

Due to changes to Public Sector Accounting Board (PSAB) standards that came into effect in 2009, municipalities are required to report on their tangible capital assets in their audited Financial Statements. The Province undertook the same change in accounting treatment in the 2002-03 fiscal year.

Under the new standards, the full cost of acquisition or construction of an asset is no longer recognized as an expenditure in the year in which it occurs. Instead, the cost of the asset is spread over the asset’s estimated useful life as amortization expense.

In order to comply with the new standards, municipalities have gathered information on the assets they own, which provides a foundation for improving asset management practices.

Since 2000, many municipalities have been participating in the Municipal Performance Measurement Program (MPMP), which tracks efficiency and effectiveness across 13 service areas. Data is collected through the Financial Information Return. In 2009, measures including amortization and interest on long-term debt were added to the existing operating cost measures. The data generated through MPMP can inform the asset management planning process.

Many associations have been developing and disseminating tools and resources to help improve municipal asset management. For example, the Ontario Good Roads Association has been working to support data collection through the Municipal DataWorks system.

Municipal DataWorks

Municipal DataWorks is a software tool that helps municipalities carry out asset management planning. It is an online database with tools to import and export infrastructure data and create flexible reports on the extent and condition of municipal infrastructure. Municipal DataWorks is managed by the Ontario Good Roads Association (OGRA).

In view of the importance of municipal bridge asset management, the Ministry of Transportation provided $1.1 million to the OGRA in 2010 and 2011 to help municipalities collect and process their bridge and culvert data and input it into Municipal DataWorks. This database now includes 15,000 bridges and large culverts from more than 340 Ontario municipalities.

The Provincial-Municipal Roads and Bridges Review also focused on the importance of improved municipal asset management. The Review was initiated following the Provincial-Municipal Fiscal and Service Delivery Review. It was a collaborative process involving members of the Association of Municipalities of Ontario (AMO), representatives from the City of Toronto, and staff from the ministries of Transportation, Infrastructure, Finance, Municipal Affairs and Housing, and Northern Development and Mines. The Roads and Bridges Review Steering Committee Final Report was released in July 2012 and is available through the AMO website.

The importance of municipal bridge inspections and maintenance was recognized in the Ontario Auditor General’s 2009 Annual Report (December 2009). A key recommendation was that the Ministry of Transportation should work with stakeholders to ensure that the condition of municipal bridges is consistently assessed, updated every two years as required, and publicly reported.

As noted on page 6, municipalities are required to inspect their bridges under the Public Transportation and Highway Improvement Act, 1990. Bridge inspections provide key information on structure condition and repair strategies and costs. This is critical for municipalities to determine their bridge infrastructure needs and priorities.

Through the province’s 2005–06 Dedicated Gas Tax Funds for Public Transportation Program, municipalities were required to develop and submit a 10-year municipal Transit Asset Management Plan. The Ministry of Transportation received 79 municipal asset management plans, satisfying the requirement for all applicable recipients. Under the federal gas tax transfer program, municipalities are required to develop or enhance an Integrated Community Sustainability Plan – a long-term plan, developed in consultation with community members, that provides direction for the community to realize sustainability objectives, including environmental, cultural, social, and economic objectives.

Good asset management has also been gaining momentum in the water sector. Operating authorities that oversee municipal residential drinking water systems must document their infrastructure maintenance, rehabilitation, and renewal programs and monitor the effectiveness of their maintenance programs as part of the quality management system required as a condition of accreditation. In addition, the Financial Plans Regulation under the Safe Drinking Water Act, 2002 requires that municipalities plan for the long-term financial viability of their drinking water system(s). The Water Opportunities Act, 2010 builds on this by setting the framework for a performance measurement regime and sustainability planning for water, wastewater, and stormwater over the lifetime of the infrastructure assets.

In the social housing sector, many municipal service managers have assessed the condition of their housing portfolios. This work has been undertaken as part of the Social Housing Renovation and Retrofit Program or previously completed assessments.

The Ministry of Municipal Affairs and Housing has worked with the Housing Service Corporation, the Centre for Asset Management, and stakeholders to provide tools to help providers and service managers undertake effective asset management planning. These tools include the publication FRAME: Fundamental Resources for Asset Management Excellence, the Asset Management Resource Kit, and access to licenses for a web-based asset management system.

Service managers across Ontario are responsible for administering approximately 230,000 units of social housing stock. To address capital repair priorities and sustainability, municipalities are encouraged to integrate asset management planning for social housing with asset management planning for other municipal infrastructure.

Municipalities need to continue to build on this work and this momentum.

Innovation

The asset management planning process is a useful venue to explore better and more cost-effective ways to deliver infrastructure services.

Alternative financing and procurement

Municipalities may be able to utilize Infrastructure Ontario’s Alternative Financing and Procurement (AFP) model to help implement projects. The AFP model brings together private and public sector expertise in a unique structure that reduces the risk of project cost increases and scheduling delays typically associated with traditional project delivery.

Costs and risks can be further reduced if the private sector is also responsible for maintenance. This delivery model, known as design-build- finance-maintain, takes a lifecycle perspective and builds effective asset management directly into the contract.

The design-build-finance-maintain model requires close coordination among all parties involved in the project, including: the designer/architect, builder, and maintenance contractor, each of whom has relevant expertise. Together, they must develop an approach that integrates capital and operating costs over a contracted period of time and minimizes the total costs. To comply with holdback provisions in the project agreement, they must also ensure the asset is in good condition at the end of the contract.

AFP and project bundling

While the AFP model is best suited to large projects, groups of smaller projects of a similar nature can be bundled and delivered by Infrastructure Ontario using the AFP model to achieve cost savings. To facilitate this, Infrastructure Ontario has established a bundling working group with industry representatives to identify best practices and guidelines.

The province has bundled projects for two large AFP contracts: the OPP Modernization project and the Highway Service Centres project.

To explore bundling of municipal bridge projects, the Ontario Good Roads Association has partnered with the Residential and Civil Construction Alliance of Ontario with the support of the Ministry of Transportation to undertake a pilot study of bridges in Wellington County.

This pilot study will provide a better understanding of the potential for municipalities to use alternative delivery approaches to minimize their long-term bridge renewal costs. Results are expected in Fall 2012.

Innovative technologies

Another potential way to “stretch” capital dollars is through the adoption of leading edge technologies. For example, the Ministry of Transportation has used rapid bridge replacement and prefabrication technology to save millions of dollars in costs as well as years in construction time.

New construction methods to replace bridges

Rapid bridge replacement is an innovative technology that allows bridges to be replaced in a matter of hours instead of months.

The state-of-the-art technology lifts out the old bridge and replaces it with a new one that has been constructed nearby. This method reduces costs, improves site safety, helps the environment, and minimizes traffic disruption. It has proved to be invaluable in replacing bridges in major urban areas in southern Ontario.

On August 18, 2010, the Ministry of Transportation removed an aging Canadian Pacific Railway (CPR) three-span bridge east of Kenora. The accelerated operations accommodated a CPR condition to have its east-west rail line shut down for no more than 12 consecutive hours. Ten hours after the last train had passed over the bridge, the railroad was ready for train traffic again – a full two hours ahead of schedule.

To save time and money, the Ministry of Transportation is using prefabricated steel structures to replace small bridges on rural, low volume roads in northern Ontario. These bridges can be replaced in less than four hours per structure and at 10% of the cost of traditional methods.

The Water Opportunities Act, 2010 will help make Ontario a North American leader in developing water technologies and services, offering our expertise to the world through the Water Technology Acceleration Project (TAP) – a technology hub that brings together industry, academics, and government to develop and promote the sector. To complement this, the Showcasing Water Innovation program is highlighting new and innovative approaches and technologies for managing drinking water, wastewater and stormwater systems.

“Green infrastructure” is one way to reduce the need for costly, large-scale solutions. It uses natural processes like infiltration and evaporation – often on a small scale close to the source – to reduce the burden on built systems. Green infrastructure is in use across Ontario. Guelph, for example, offers a $2,000 rebate for large capacity rainwater harvesting systems. As well as reducing costs, green infrastructure generates other benefits, which include removing undesirable chemicals from stormwater, increasing green space in urban environments, converting carbon dioxide into oxygen, and providing natural habitat.

Better integrated infrastructure planning and land use planning

Municipalities can also consider how their “built form” affects infrastructure needs. Denser municipalities, for example, require shorter lengths of roads, sidewalks and pipes for the same number of residents. This can result in lower costs per household. A number of studies by IBI Group, the Brookings Institution and the Canada Mortgage and Housing Corporation have found that compact, smart growth development saves up to 30% on capital costs and up to 15% on operating costs for infrastructure compared to traditional development patterns.

Effective land use planning helps to establish a foundation for municipalities to align infrastructure investments with growth management, optimize the use of existing, planned, and new infrastructure, co-ordinate water and wastewater services, and promote green infrastructure and innovative technologies.

For municipalities anticipating major growth, undertaking master infrastructure plans in conjunction with an official plan update can provide a sound basis for considering the most cost-effective way to plan for new infrastructure. The province’s newly published Transit- Supportive Guidelines provide practical information to help optimize transit investment. These guidelines are available through the Ministry of Transportation website.

Integration with financial planning

As noted on page 5, financing strategies are a key component of a detailed asset management plan. As such, asset management planning must be integrated with financial planning and budgeting.

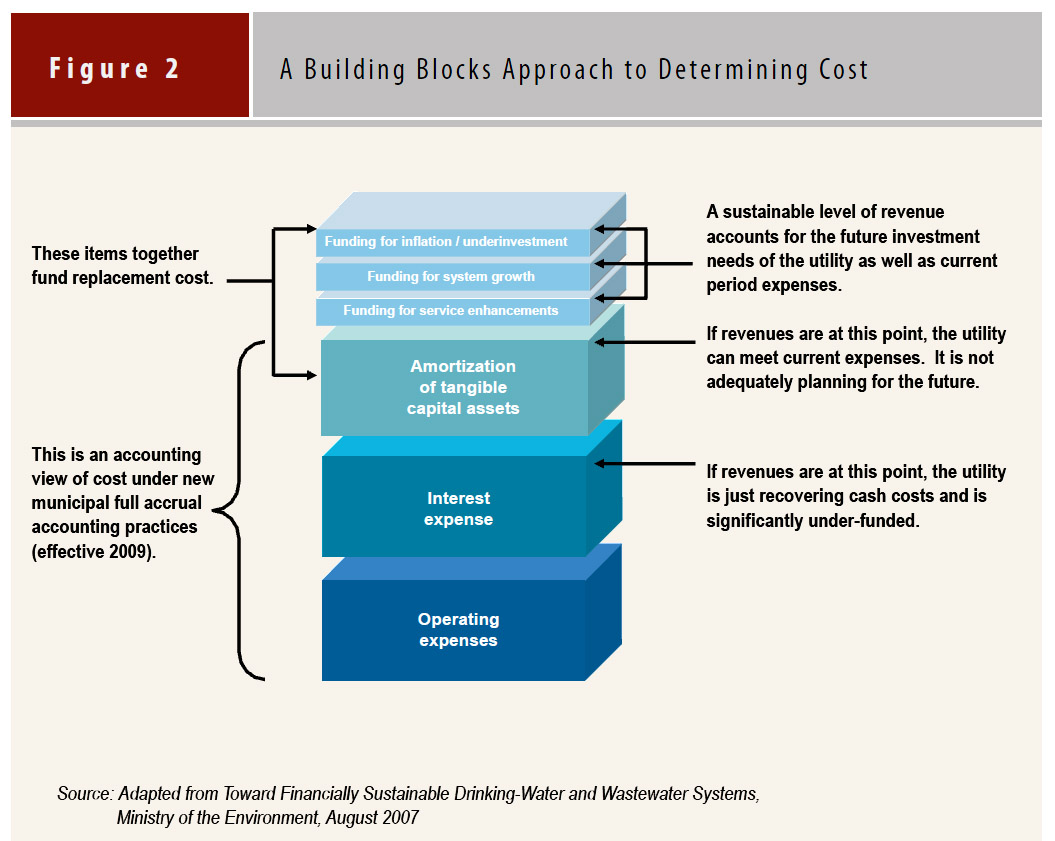

Some of the costs associated with planning, building, and maintaining infrastructure may be classified as operating expenses. Figure 2 shows a “building block” approach to identifying costs that includes four distinct components. While the diagram reflects an approach for water and wastewater systems, it has direct application to other types of municipal infrastructure. Municipalities may wish to consider this framework when estimating costs associated with asset management strategy options, and the corresponding funding needed to support service sustainability over time.

Figure 2: A Building Blocks Approach to Determining Cost.

The figure shows 6 building blocks:

- Funding for inflation / underinvestment

- Funding for system growth

- Funding for service enhancements

- Amortization of tangible capital assets

- Interest expense

- Operating expenses

The first 3 building blocks: Funding for inflation / underinvestment, Funding for system growth and Funding for service enhancements have a sustainable level of revenue accounts for the future investment needs of the utility as well as current period expenses. They also fund replacement cost.

- Block 4 - Amortization of tangible capital assets states that if revenues are at this point, the utility can meet current expenses. It is not adequately planning for the future.

- Block 5 – Interest expense states that if revenues are at this point, the utility is just recovering cash costs and is significantly under-funded.

- Blocks 4 – 6 are accounting views of cost under new municipal full accrual accounting practices (effective 2009).

Source: Adapted from Toward Financially Sustainable Drinking-Water and Wastewater Systems, Ministry of the Environment, August 2007

From an accounting perspective, the focus is on the financial position of a municipality at a particular point in time and the changes over the accounting period. In contrast, asset management planning should not only focus on what has happened in the past, but also take a forward looking approach to planning for long-term financial sustainability.

One approach to estimating required capital spending could be to assume that assets will need to be replaced at the end of their lives. This is a reasonable assumption for estimating total funding needs. Asset management plans, however, are still needed to help decide when to replace specific individual assets and to help allocate funds within an overall capital budget. Replacement of any individual asset or group of assets should be driven by a detailed analysis of that asset or group. It should not be automatically dictated by financial plan assumptions.

For services to be sustainable, a financing plan needs to be in place to implement the actions identified in the asset management plan. Funding for asset management plans should come from a variety of sources – including property taxes, user fees, debt issuance, and drawing on reserves. It may not be advantageous for large, onetime capital expenditures to be funded from current revenues alone. Municipalities need to plan their reserves and debt issuance accordingly.

Kitchener’s new stormwater user fee

The City of Kitchener transferred stormwater management funding from property taxes to a user-fee program, effective January 1, 2011. Rates are based on property type and size of impervious area, to account for the varying degrees of water runoff generated from properties that use the system. The average single dwelling homeowner is charged approximately $9.73 per month for stormwater management.

This funding model allows the city to dedicate dollars specifically to stormwater management – a service that has been consistently underfunded through the tax base.

A recent update to the model will offer property owners who actively decrease the volume of stormwater and pollution coming off their properties a credit of up to 45% of their bill.

Enhancing the asset management

The current state of asset management planning varies among municipalities. Regardless of whether a municipality is beginning to develop a plan or reviewing an existing one, the following actions may help to create a successful outcome.

Direction and support

- Obtain a Council resolution that directs staff to develop an asset management plan.

- Designate a project champion within the municipal administration and another on Council.

- Establish a Working Group or Steering Committee to engage the appropriate municipal departments in the process

- Ensure that engineering, finance and other appropriate representatives are included.

Public engagement

- Engage the public to help envision what the municipality will look like in the future and the infrastructure needed to support it.

- Assist the engagement process by identifying priority projects and developing costing scenarios.

- Be open to a conversation about prioritization and the difficult choices that sometimes need to be made.

External support and collaboration

- Consider if advice from external experts would help Council to make better informed decisions on the asset management plan.

- Examine the advantages of potential partnerships with neighbouring municipalities. Partnerships could be as simple as sharing resources and bundling multiple projects into one procurement - or more complex arrangements involving consolidation of infrastructure services.

An open and ongoing process

- Ensure that asset management plans are clear and available to the public.

- Monitor and report on the implementation of asset management plans at the Council and staff levels.

- View asset management plans as “living” documents that require continuous updates and improvements.

Part 3: The elements of a detailed Asset Management Plan

An asset management plan is a strategic document that states how a group of assets is to be managed over a period of time. The plan describes the characteristics and condition of infrastructure assets, the levels of service expected from them, planned actions to ensure the assets are providing the expected level of service, and financing strategies to implement the planned actions. A detailed asset management plan has the following sections:

- executive summary

- introduction

- state of local infrastructure

- expected levels of service

- asset management strategy

- financing strategy

Future provincial capital funding will be conditional on municipalities ensuring that their asset management plans include, at minimum, all of the content described here. All data and analysis supporting the asset management plan (including what is specified in this document and any additional work the municipality chooses to undertake) must be documented and kept on file.

This guide is intended to be a starting point for municipal asset management planning. Municipalities are responsible for tailoring their asset management plans to their unique needs and ensuring that all of the relevant expertise has been brought to bear in developing them.

Through the web portal, municipalities can access a range of resources to help them develop their asset management plans.

Executive summary

The executive summary is typically the final section to be prepared, and provides a succinct overview of the plan.

Introduction

The introduction:

- explains how the goals of the municipality are dependent on infrastructure. This could include discussing how infrastructure assets support economic activity and improve quality of life. The municipality’s goals may already be set out in documents, including the strategic plan and/or the Official Plan, or may need to be developed in consultation with residents.

- clarifies the relationship of the asset management plan to municipal planning and financial documents (e.g. how the plan impacts the budget, Official Plan and Infrastructure Master Plan).

- describes to the public the purpose of the asset management plan (i.e. to set out how the municipality’s infrastructure will be managed to ensure that it is capable of providing the levels of service needed to support the municipality’s goals).

- States which infrastructure assets are included in the plan. Best practice is to develop a plan that covers all infrastructure assets for which the municipality is responsible. At a minimum, plans should cover roads, bridges, water and wastewater systems, and social housing.

- identifies how many years the asset management plan covers and when it will be updated. At a minimum, plans must cover 10 years and be updated regularly. Best practice is for plans to cover the entire lifecycle of assets.

- describes how the asset management plan was developed — who was involved, what resources were used, any limitations, etc.

- identifies how the plan will be evaluated and improved through clearly defined actions. Best practice is for actions to be short-term (less than three years) and include a timetable for implementation.

State of local infrastructure

This section of the plan summarizes in one or more tables:

- asset types (e.g. urban arterial road, rural arterial road, watermains) and quantity/extent (e.g. length in kilometres for linear assets).

- financial accounting valuation and replacement cost valuation. Financial valuation uses historical costs and depreciation assumptions. Replacement cost valuation is forward-looking and accounts for expected inflation, changes in technology and other factors.

- asset age distribution and asset age as a proportion of expected useful life.

- asset condition (e.g. proportion of assets in “good,” “fair” and “poor” condition). Asset condition must be assessed according to standard engineering practices. For bridge structures, condition is based on an analysis of bridge inspection reports.

This section also discusses how and when information regarding the characteristics, value, and condition of assets will be updated.

This section is supported by:

- an inventory database of infrastructure assets covered by the plan, which includes basic asset information (e.g. asset type/ class, physical description, location, expected useful life, etc.) and information that will require regular updates (e.g. replacement cost, condition, performance, etc.). The database could take the form of a simple spreadsheet or a more complex system supported by dedicated asset management software, such as Municipal DataWorks.

- records of all assumptions, which could be incorporated into the asset inventory or recorded in stand-alone documentation.

- a data verification policy and a condition assessment policy that sets out when and how asset information will be verified and when and how assets will be assessed to determine their condition. This policy must be consistent with provincial requirements – for instance, the requirement that municipal bridges be inspected every two years.

Desired levels of service

While the introduction of an asset management plan explains in a general way how the goals of the municipality rely on infrastructure, the levels of service section is much more detailed. This section:

- defines levels of service through performance measures, targets and timeframes to achieve the targets if they are not already being achieved. For example, levels of service for a water system could include:

- “X” breaks per 100 km of watermain per year are acceptable;

- Watermain breaks will be repaired within “X” hours of initiation of repair, 95% of the time;

- Customer complaints will be responded to within 24 hours;

- The meeting of all regulatory requirements.

- discusses any external trends or issues that may affect expected levels of service or the municipality’s ability to meet them (e.g., new accessibility standards, climate change impacts).

- shows current performance relative to the targets set out. A table may be useful for this.

This section is supported by documentation that specifies which performance measures are associated with which assets, current performance and expected performance over the planning period, as well as all assumptions. One way to link performance measures and current/expected performance to the relevant assets is through the asset inventory database.

Asset management strategy

The asset management strategy is the set of planned actions that will enable the assets to provide the desired levels of service in a sustainable way, while managing risk, at the lowest lifecycle cost (e.g., through preventative action). This section of the asset management plan:

- summarizes planned actions, including:

- non-infrastructure solutions – actions or policies that can lower costs or extend asset life (e.g., better integrated infrastructure planning and land use planning, demand management, insurance, process optimization, managed failures, etc.).

- maintenance activities – including regularly scheduled inspection and maintenance, or more significant repair and activities associated with unexpected events.

- renewal/rehabilitation activities – significant repairs designed to extend the life of the asset. For example, the lining of iron watermains can defer the need for replacement.

- replacement activities – activities that are expected to occur once an asset has reached the end of its useful life and renewal/ rehabilitation is no longer an option.

- disposal activities – the activities associated with disposing of an asset once it has reached the end of its useful life, or is otherwise no longer needed by the municipality.

- expansion activities (if necessary) – planned activities required to extend services to previously unserviced areas - or expand services to meet growth demands.

- discusses procurement methods. To ensure the most efficient allocation of resources, best practice is for a number of delivery mechanisms to be considered — such as working with other municipalities to pool projects and resources, or considering an AFP model. As previously mentioned, the design-build-finance maintains AFP model takes a lifecycle perspective and builds effective asset management directly into the contract.

- includes an overview of the risks associated with the strategy (i.e. ways the plan could fail to generate the expected service levels) and any actions that will be taken in response.

Procurement

Municipalities should have procurement by-laws in place to serve as the basis for considering various delivery mechanisms. The Ministry of Municipal Affairs and Housing has produced a procurement bylaw development guideline that provides best practices and general information on content and considerations for municipal procurement policies. This guideline is available through the Ministry of Municipal Affairs and Housing website.

Undertaking options analysis is necessary to develop the strategy section of the asset management plan. This analysis compares different actions that would enable assets to provide the needed levels of service.

Options must be compared based on:

- lifecycle cost – the total cost of constructing, maintaining, renewing and operating an infrastructure asset throughout its service life. Future costs must be discounted and inflation must be incorporated. Municipalities need to use appropriate indices to calculate discount or inflation rates. For example, planned maintenance projects could use a standard inflation measure, while large capital projects may require a more specific measure that better reflects changes in construction costs.

- an assessment of all other relevant direct and indirect costs and benefits associated with each option. Examples include:

- direct benefits and costs:

- efficiencies and network effects (such as savings in wastewater treatment due to conservation and efficiency improvements to the water system or savings of time and vehicle operating costs for users of transportation infrastructure).

- investment scheduling to appropriately time expansion in asset lifecycles (for example, consider delaying the resurfacing of road assets before an imminently planned expansion to save costs and minimize waste).

- safety (accident reduction and impact on both property damage and injury/fatalities).

- environmental impacts such as greenhouse gas emissions or nutrient loading.

- vulnerability to climate change impacts or climate change adaptation.

- indirect Benefits and Costs

- municipal wellbeing and health.

- amenity values.

- value of culturally or historically significant sites.

- municipal image.

- direct benefits and costs:

- an assessment of the risks associated with all potential options. Each option must be evaluated based on its potential risks, using an approach that allows for comparative analysis. Risks associated with each option can be scored based on quantitative measures when reasonable estimates can be made of the probability of the risk event happening and the cost associated with the risk event. Qualitative measures can be used when reasonable estimates of the probability and the cost associated with the risk event cannot be made.

Risk management in Peel Region

The Region of Peel has developed a risk-centric methodology to optimize asset management decision-making at the enterprise level. The optimized decision model balances risks to services at desired levels with the cost of mitigation to show where the risk reduction potential per dollar is highest. For example, the level of service for water mains could be allowed to remain at 90% of the desired level with low risk whereas more could be done to mitigate risk at lower cost by investing in higher risk status assets such as social housing or road pavements.

Source: Grace McLenaghan, “Optimized Decision Modeling for Organizational Asset Management,” Public Sector Digest (September 2010)

Opportunities to save resources by coordinating solutions to multiple problems must be explored. The asset management strategy is the set of actions that, taken together, has the lowest total cost — not the set of actions that each has the lowest cost individually. All decisions made regarding the set of preferred solutions and the person making the decision must be recorded.

Integrated planning to optimize lifecycle costs

A common strategy is to coordinate capital spending across multiple assets. A good example is coordinating water and wastewater repair/ replacement with municipal road replacement.

Municipal roads periodically need to be rebuilt, and the associated schedules are part of the municipal planning cycle. If there is a good possibility that a watermain or sewermain will fail or start to provide degraded service – during the life of the road that is being rebuilt, significant cost savings can be achieved by replacing the watermain or sewermain at the same time.

Source: Toward Financially Sustainable Drinking-Water and Wastewater Systems, Ontario Ministry of the Environment (2007)

Financing strategy

As noted on page 9, having a financial plan is critical for putting an asset management plan into action. In addition, by having a strong financial plan, municipalities can demonstrate that they have made a concerted effort to integrate asset management planning with financial planning and budgeting and to make full use of all available infrastructure financing tools.

This section of a detailed asset management plan:

- shows yearly expenditure forecasts broken down by:

- non-infrastructure solutions

- maintenance activities

- renewal/rehabilitation activities

- replacement activities

- disposal activities

- expansion activities (if necessary)

- provides actual expenditures for these categories from the previous two to three years for comparison purposes.

- gives a breakdown of yearly revenues by confirmed source (i.e. loans and senior government grants should not be included unless an agreement has been executed).

- discusses key assumptions and alternative scenarios where appropriate.

- identifies any funding shortfall relative to financial requirements that cannot be eliminated by revising service levels, asset management and/or financing strategies, and discuss the impact of the shortfall and how the impact will be managed.

This section is supported by documentation explaining how the expenditure and revenue forecasts were developed. Expenditure forecasts must be consistent with the options analysis supporting the strategy section of the asset management plan. Revenue forecasts must be documented separately, along with the assumptions made and alternative scenarios. Ten years is considered a minimum timeframe for expenditure and revenue forecasts. However, a best practice is to use a forecast period that covers the entire lifecycle of assets.

Part 4: Conclusion

For many municipalities, improving asset management will require a significant effort. This effort is worthwhile. Informed and timely decisions will help municipalities to optimize investments, save money in the long run, and better manage risks. Improved municipal asset management will also help ensure that limited provincial resources are directed to the most critical needs.

Through the new Municipal Infrastructure Investment Initiative, the province made asset management entitlement funding available in 2012–13 to small municipalities, Northern Ontario Local Services Boards with water/wastewater systems, and municipal service managers that are responsible for a small number of social housing units.

While improved asset management by municipalities is an important first step, the municipal infrastructure strategy will be a long-term, cooperative effort among all three orders of government. The province looks forward to a continuing partnership on infrastructure issues with municipalities and the federal government.

Chart Descriptions

Chart 1: Ontario Per Capita in Net Public Capital Stock

Chart 1 is a bar graph showing the changes in net stock per capita as averaged over five year periods from 1955-2009. The net book value is adjusted to 2002 dollars per person. The graph is split into 3 sections.

- Era of Visionary Investment between the years of 1968-1976

- Era of Neglect between the years of 1978-2000

- Era of Renewal between the years of 2001-2011

Figure 1: Small but Timely Renewal Investments Save Money

This chart shows the high cost of neglect. If the condition of the asset is allowed to deteriorate to the point where it must be replaced, the cost is $60 million every 30 years. In contrast, if smart asset management is undertaken and proactive rehabilitation investments are made, the cost would be $10 million every 15 years.

Figure 2: A Building Blocks Approach to Determining Cost

The figure shows 6 building blocks:

- Funding for inflation / underinvestment

- Funding for system growth

- Funding for service enhancements

- Amortization of tangible capital assets

- Interest expense

- Operating expenses

The first 3 building blocks: Funding for inflation / underinvestment, Funding for system growth and Funding for service enhancements have a sustainable level of revenue accounts for the future investment needs of the utility as well as current period expenses. They also fund replacement cost.

- Block 4 – Amortization of tangible capital assets states that if revenues are at this point, the utility can meet current expenses. It is not adequately planning for the future.

- Block 5 – Interest expense states that if revenues are at this point, the utility is just recovering cash costs and is significantly under-funded.

- Blocks 4 – 6 are accounting views of cost under new municipal full accrual accounting practices (effective 2009).