We've moved this content over from an older government website. We'll align this page with the ontario.ca style guide in future updates.

Non-Resident Speculation Tax collected

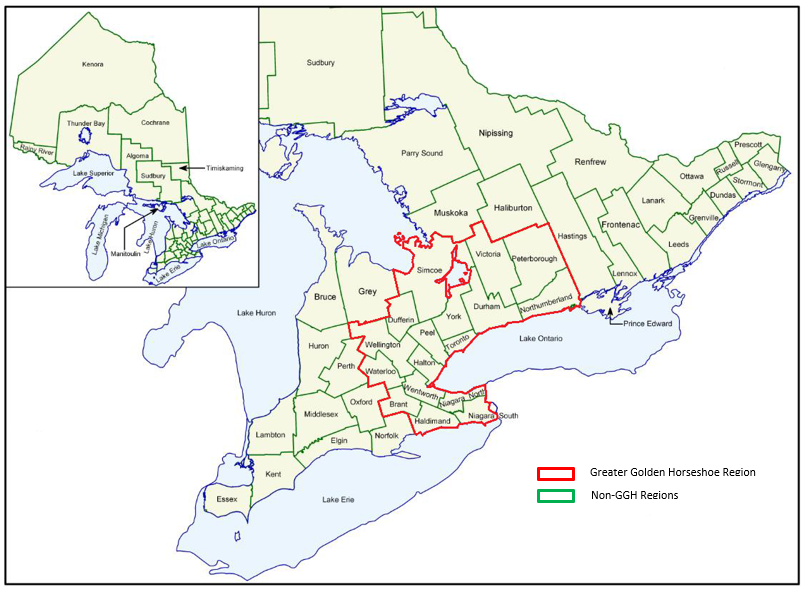

On April 21, 2017, the Province introduced the Non-Resident Speculation Tax (NRST), which at the time was a 15 per cent tax on the purchase or acquisition of an interest in residential property located in the Greater Golden Horseshoe Region (GGH) by foreign entities (individuals who are not citizens or permanent residents of Canada and foreign corporations) and taxable trustees. On March 30, 2022, the NRST rate was increased to 20 per cent, and its application was expanded provincewide. On October 25, 2022, the NRST rate was further increased to 25 per cent. Moving forward, the government is taking further action to strengthen the NRST with amendments to support compliance and improve fairness.

The NRST applies in addition to the general land transfer tax in Ontario.

Specifically, the NRST applies on the transfer of land which contains at least one and not more than six single family residences. Examples of land containing one single family residence include land containing a detached house, a semi‑detached house, a townhouse or a condominium unit. As of March 27, 2024, standalone purchases of parking units and storage units in a condominium complex are also subject to NRST.

This report is based on the NRST collected on applicable transactions. The table in this report is for payments made to the Ministry of Finance between April 21, 2017, and December 31, 2025, and includes a breakdown of the NRST collected based on Land Registry Offices (LROs).

Note: The amount of NRST collected should not be used to correlate or estimate foreign transactions or activity, as some foreign transactions were subject to transitional relief or exempt from NRST. Please see Land Transfer Tax - Additional Information Collection - Purchases by Foreign Entities.

For more information on the NRST and its exemptions and rebates, refer to the Non-Resident Speculation Tax webpage bulletin.

Non-Resident Speculation Tax Collected – April 21, 2017 to December 31, 2025

Note: The figures in this table reflect the total NRST paid to the Ministry. Therefore, these figures may include amounts that are currently subject to an application for a rebate or refund, or may (in the future) be subject to an application for a rebate or refund.

| Land Registry Offices (LROs) | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|---|---|---|---|

| GGH Total | 156.7 | 196.1 | 170.4 | 168.1 | 167.8 | 184.0 | 71.3 | 81.5 | 38.6 |

| Brant | 0.0 | 0.2 | 0.0 | 0.5 | 0.0 | 0.0 | 0.2 | 1.0 | 0.2 |

| Dufferin | 0.0 | 0.3 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Durham | 1.5 | 2.3 | 2.8 | 2.0 | 2.7 | 3.6 | 1.0 | 0.5 | 0.5 |

| Halton | 7.7 | 13.2 | 9.2 | 13.0 | 13.9 | 16.4 | 6.8 | 3.9 | 1.2 |

| Niagara South & North | 3.1 | 3.9 | 4.3 | 4.7 | 3.7 | 3.2 | 1.3 | 0.7 | 0.5 |

| Peel | 10.9 | 14.8 | 10.1 | 12.6 | 13.9 | 11.8 | 4.9 | 2.2 | 2.0 |

| Peterborough | 0.4 | 0.5 | 0.0 | 0.0 | 0.0 | 0.8 | 0.1 | 0.2 | 0.2 |

| Simcoe | 0.9 | 0.8 | 1.6 | 0.7 | 3.8 | 2.3 | 1.2 | 0.4 | 0.7 |

| Toronto | 76.4 | 105.1 | 88.7 | 83.1 | 76.3 | 91.5 | 28.6 | 54.0 | 22.4 |

| Waterloo | 5.2 | 4.6 | 6.8 | 6.1 | 6.8 | 6.4 | 1.8 | 1.5 | 1.2 |

| Wellington | 0.0 | 1.1 | 1.6 | 1.2 | 1.4 | 1.3 | 0.4 | 0.1 | 0.2 |

| Wentworth | 2.2 | 4.3 | 3.3 | 3.4 | 3.8 | 2.2 | 1.0 | 0.7 | 0.6 |

| York | 48.0 | 44.7 | 41.5 | 40.2 | 40.9 | 43.5 | 23.8 | 16.0 | 8.3 |

| Other GGH Regions | 0.4 | 0.3 | 0.5 | 0.5 | 0.5 | 0.8 | 0.2 | 0.3 | 0.7 |

| Non-GGH Total | N/A | N/A | N/A | N/A | N/A | 16.3 | 12.7 | 14.4 | 16.4 |

| Algoma | N/A | N/A | N/A | N/A | N/A | 0.9 | 0.2 | 0.8 | 0.6 |

| Bruce | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | 0.6 |

| Essex | N/A | N/A | N/A | N/A | N/A | 1.6 | 0.7 | 0.5 | 0.2 |

| Kenora | N/A | N/A | N/A | N/A | N/A | 0.6 | 1.3 | 1.4 | 1.0 |

| Leeds | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | 1.4 |

| Middlesex | N/A | N/A | N/A | N/A | N/A | 2.7 | 1.1 | 0.5 | 0.2 |

| Muskoka | N/A | N/A | N/A | N/A | N/A | 1.2 | 0.6 | 2.2 | 2.2 |

| Ottawa | N/A | N/A | N/A | N/A | N/A | 4.6 | 3.3 | 4.0 | 2.1 |

| Parry Sound | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | 1.5 |

| Rainy River | N/A | N/A | N/A | N/A | N/A | 0.5 | 0.9 | 1.0 | 0.7 |

| Sudbury | N/A | N/A | N/A | N/A | N/A | 1.1 | 0.2 | 0.3 | 0.5 |

| Thunder Bay | N/A | N/A | N/A | N/A | N/A | 0.0 | 0.0 | 0.2 | 0.6 |

| Other Non-GGH Regions | N/A | N/A | N/A | N/A | N/A | 3.1 | 4.5 | 3.3 | 4.7 |

| Ontario Total | 156.7 | 196.1 | 170.4 | 168.1 | 167.8 | 200.3 | 84.0 | 95.9 | 55.0 |

Note: Numbers in table above may not add due to rounding.

Glossary

| Term | Definition |

|---|---|

| Additional Information Collection (Prescribed Information for the Purposes of Section 5.0.1) | On April 24, 2017 the Province began collecting additional information to better understand trends in the housing market through the land transfer tax (LTT) system. All persons who purchase or acquire land in Ontario that contains at least one and not more than six single family residences, or agricultural land, are required to provide this additional information. For more information, refer to the Prescribed Information for the Purposes of Section 5.0.1. |

| Foreign corporation | Means a corporation that is one of the following:

|

| Foreign entity | Means a foreign corporation or a foreign national. |

| Foreign national | An individual who is a foreign national as defined in subsection 2 (1) of the Immigration and Refugee Protection Act (Canada), but does not include a person registered as an Indian under the Indian Act (Canada). |

| Greater Golden Horseshoe Region (GGH) | Refers to the area of land comprised of the geographic areas of the following municipalities:

|

| Land Registry Office (LRO) | LROs are managed by the Ministry of Public and Business Service Delivery and Procurement and allow persons to register and search official private property records using Ontario’s land registration system. |

| Land Transfer Tax (LTT) | The LTT is a broad-based tax imposed on persons acquiring land, or a beneficial interest in land, in Ontario with few exceptions. LTT is payable to the Province when the transfer is registered under the Land Titles Act or the Registry Act, as applicable. If the acquisition of an interest in land is not registered, LTT is payable directly to the Province in respect of the unregistered disposition of a beneficial interest in land, within 30 days after the transaction closing date. |

| Nominee | Means a foreign national who is nominated under the Ontario Immigrant Nominee Program. |

| Permanent resident of Canada | Means a person who has acquired permanent resident status and has not subsequently lost that status under section 46 of the Immigration and Refugee Protection Act (Canada). |

| Protected person | Means a foreign national on whom refugee protection is conferred under section 95 of the Immigration and Refugee Protection Act (Canada). |

| Single family residence | Means a unit or proposed unit under the Condominium Act, 1998 or a structure or part of a structure that is designed for occupation as the residence of a family, including dependents or domestic employees of a member of the family, whether or not rent is paid to occupy any part of it and whether or not the land on which it is situated is zoned for residential use and,

For example: a detached and semi‑detached house, duplex, freehold townhouse, condominium townhouse, condominium apartment, and cottage. |

| Taxable trustee | Means a trustee of:

Taxable trustee does not include a trustee acting for the following types of trusts:

|

Appendix A: Ontario – Land Registry Offices

Appendix B: NRST and Additional Information Collection – Comparison

| Item | NRST | Additional Information Collection |

|---|---|---|

| Date of Implementation | April 21, 2017 | April 24, 2017 |

| Transitional Provisions | Transitional relief provisions are available for eligible transactions regarding the general application of the NRST, as well as the applicable tax rate. Refer to the NRST webpage bulletin for more information. | N/A |

| Geographic Area | All of Ontario (applied only to the Greater Golden Horseshoe Region prior to March 30, 2022) | All of Ontario |

| Type of Property | Land that contains:

| Land that contains:

|

| Applicable Transferees (for example, Purchasers) | The data will only show those who were subject to the tax (foreign entities, and taxable trustees).

| All persons who purchase or acquire the applicable land (see above) in Ontario. This includes the following:

|

| Transferees Excluded or Exempt |

|

|

Note: For exclusions relating to trustees of mutual fund trusts, REITs, and SIFT trusts, the trustee must exclusively hold title (or must hold title with similar trustees or other eligible persons).

Contact us

We are committed to providing accessible customer service. On request, we can arrange for accessible formats and communication supports. If you have questions, requests, or need help locating a document, please contact us.

Footnotes

- footnote[1] Back to paragraph LRO boundaries may not coincide with municipal, county or district boundaries.

- footnote[2] Back to paragraph Combined LROs due to low transaction counts.

- footnote[3] Back to paragraph Prior to March 30, 2022, the NRST applied only in the GGH.

- footnote[4] Back to paragraph In order to be eligible for an exemption from the NRST, the purchaser must meet all requirements (for example, certification to occupy the land as a principal residence), and the land must be held exclusively by the transferee and their spouse (and potentially other eligible persons).